U.S. commercial real estate investment volume rose by 10% year-over-year in Q2 2022 to $167 billion. Multifamily was the leading sector with $78 billion in Q2 volume, due to the resilience shown by this asset class as well as continued housing shortage. Industrial and logistics properties had $32 billion in total volume for the quarter; the pandemic not only created a boom in online retail, but also caused a permanent migration of consumer behavior towards online retail. In third place was office properties with $24 billion in transaction volume, driven by workers returning to the office.

While a sharp rise in interest rate will generally drive down real estate prices, there are many other factors at play. The Federal Reserve’s multiple increases to its target rate have both short-term and long-term effects. In the short-term, rate increases will discount the prices of real estate assets, as the market now demands a higher rate of return on those assets for sale given the same rental income. Furthermore, those assets whose mortgages are structured with variable rate without an interest cap built in will be facing increased monthly mortgage payments, which cut into net operating income and asset value. Lastly, many lenders will experience a sudden increase in their cost of capital (borrowing costs), which may cause some lenders to temporarily pull back from lending altogether. Nonetheless, the long-term impacts to the industry are positive – once the interest rate increases implemented by the Fed takes effect in reducing inflation, the U.S. economy should emerge out of recession relatively quickly and return to growth. Comparatively this is a manageable short-term sacrifice in order to prevent a much more painful longterm decline.

U.S. Commercial Real Estate Investment Volume by Quarter

U.S. Commercial Real Estate Investment Volume by Sector

U.S. Commercial Real Estate Investment Volume by Market (Last 4 Quarters)

U.S. Real Estate – Multifamily Market

In Q2 we saw an increase in the overall U.S. multifamily vacancy rate to 3.1% from 2.4% in Q1. This was the first increase in five quarters, but this vacancy level is still well below the long-term average of 4.9%. The increase was largely a result of high inflation and loss of consumer confidence, causing families to consolidate rather than rent separate units. This increase seemed to be consistent across all classes of multifamily assets in both city centers as well as surrounding areas. Not surprisingly, the average rent per unit also reached a historic new high of $2,080 per month, buoyed by continued inflation and low unemployment rate.

U.S. Multifamily Vacancy Rate and YoY % Change

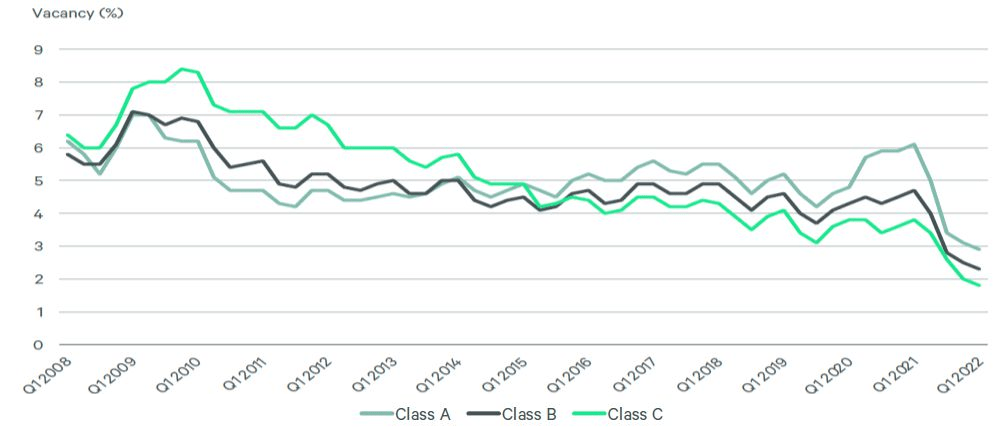

U.S. Multifamily Vacancy Rate by Class

U.S. Multifamily Monthly Rent and YoY % Change

U.S. Real Estate – Commercial Retail Market

Total retail sales growth dropped to 3.8% even during an inflationary environment, a sign that the recovery in the retail sector is nearing its end, and consumer confidence may be eroding and hurting spending. Retail space absorption fell by 40% compared to Q1 and fell by 20% compared to Q2 2021, also indicative of the end of the retail recovery. Average retail asking rent grew by 2.4% year-over-year, the highest increase in more than 5 years, but it is still lagging the wage growth of 4.4% year-over-year.

U.S. Consumer Retail Sales Growth and YoY% Change

U.S. Retail Sales by Category

U.S. Retail Vacancy Rate by Property Type

U.S. Retail Average Asking Rent

Data Sources: CBRE Research, CBRE Econometric Advisors, CoStar Realty Information Inc., Bloomberg, Zillow Group, Redfin

For additional information, please contact: Grandway Group Email: Info@grandway.com Tel: +1 626-357-1200

Markets in the first half of 2022 have been generally disappointing, with sharply rising inflation and interest rates, falling stock prices, a rampant wave of Omicron virus, and Russia’s shocking and brutal invasion of Ukraine. These factors, combined with a partisan political environment, have driven consumer sentiment down to its lowest level on record. On the positive side, however, while real GDP shrank in Q1, recent monthly data suggested solid growth during the course of Q2 as the Omicron variant subsided and spending picked up in the industries that were impacted the most by the pandemic such as travel, restaurants, leisure, and entertainment.

Entering Q3, several factors continue to weigh on economic momentum. After two years of record stimulus, the U.S. economy is facing significant fiscal slowdown, with the federal budget deficit likely to fall from 12.4% of GDP in 2021 to less than 4% of GDP this year, which would pose the single largest decline since the end of World War II. This decline reflects an end to stimulus checks, enhanced unemployment benefits, enhanced child tax credits, and a host of other programs that were supporting lower and middle-income households during the pandemic. In addition, a surge in 30-year mortgage rates is weighing on the housing sector and an 8%+ rise in the trade-weighted dollar year-to-date is impeding U.S. exports. All of this, combined with collapsing consumer confidence, has raised the risk that the U.S. economy would fall into recession in the near term.

The U.S. Federal Reserve has two main mandates: to control inflation and to control unemployment rate. As expected, the extraordinarily strong labor market and persistent inflation have pushed the Fed to adopt a much more hawkish stance. At its June meeting, the Fed increased the federal funds rate by 0.75%, following increases of 0.25% in March and 0.50% in May. In addition, the median expectation among FOMC members is for the rate to be further increased by 1.75% this year and by 0.5% next year, bringing the federal funds rate to a range of 3.25%-3.50% by the end of 2022 and 3.75%-4.00% by the end of 2023. On quantitative tightening, the Fed is also increasing the pace of reduction of their massive bond holdings to up to $95 billion/month by September.

Notably, the Fed expects inflation will fall towards its 2% target over the next few years. The latest Federal Reserve forecast suggests that annual PCE core inflation may fall from its current 4.8% to 4.3% by Q4 2022, to 2.7% by Q4 2023, and eventually to 2.3% by Q4 2024. Futures markets seem to generally agree with the Fed’s forecasts of the federal funds rate for the rest of 2022, but it appears that market participants expect the Fed to ease policy starting in the first half of 2023, suggesting the possibility that the aggressive moves by the Fed may tip the economy into recession and cause the Fed to again start easing monetary policy.

The labor market in the U.S. continues to be a bright spot. In an otherwise gloomy economic environment, the unemployment rate remained at 3.6% for the third consecutive month in May, just 0.1% above its 50- year low in 2019. There continues to be massive excess demand for labor, with roughly 5.45 million more job openings than unemployed workers in May. This excess demand should fade over the next few months, reflecting slowing economic momentum and diminished business confidence. However, it is likely to keep wage gains elevated and hopefully encourage an increase in labor force participation, particularly as an aging baby-boom generation and limited immigration continue to reduce labor supply.

High inflation in the U.S. has been a result of strong consumer spending combined with supply shortages across major sectors of the economy. More recently, this has been amplified by a general recovery in airfares, hotel rates, and rents from their pandemic lows. Inflation has been further exacerbated by continued supply chain problems due to the Russian invasion of Ukraine and China’s attempts to maintain a “zero-COVID” policy. By the end of 2022, we do expect some of the supply-driven issues to fade, alleviating the current inflation. However, the longer high inflation persists, the stickier it gets and the more likely core PCE inflation would remain above 3% year-over-year throughout 2022 and 2023. The potential persistence of inflation above the Fed’s 2% target over the next two years will have major implications for monetary policy.

Following a spectacular 2021, during which S&P 500 earnings-per-share (EPS) rose by 70%, profits are growing much more slowly in 2022. In the first quarter, EPS rose just 4.2% year-over-year and analysts are currently expecting an increase of less than 8% for the entire year 2022.

However, even these estimates may be optimistic. Companies are facing a number of different headwinds – rising wages, higher commodity prices and input costs, higher interest rates and slowing nominal sales growth. While energy companies will continue to benefit from high margins, in most other industries these headwinds are likely to cut into profits. A much higher dollar will also hinder exports and overseas sales, while recession concerns could cause company managements to cut discretionary expenses.

A recession would certainly lead to a sharp decline in corporate profits. However, if this eventually leads to less wage pressure and easier monetary policy, it could create a better long-term business environment all around. Furthermore, gridlock in Washington and the prospect of a Republican takeover of Congress after midterm elections later this year suggest that we are unlikely to see an increase in corporate taxes, suggesting that after-tax profit margins are likely to remain at the current high levels.

The global economy presents a mixed picture entering the second half of 2022. On the positive side, the effects of the pandemic are fading in most parts of the world due to widespread immunity gained from both inoculation, infection, and virus variants becoming less deadly. However, the Chinese economy continues to be impacted by the pandemic as it struggles to sustain a “zero-Covid” policy. European economies are also being badly impacted by much higher energy prices resulting from the war in Ukraine.

Inflation has become a global concern and most central banks are tightening policy to combat it. While we do not expect this to result in a global recession, it should slow the pace of economic recovery around the world. This should, however, relieve some of the pressure on commodity prices if 2023 sees positive economic growth but less inflation around the world.

Data Sources: CBRE Research, CBRE Econometric Advisors, CoStar Realty Information Inc., Bloomberg, Zillow Group, Redfin

For additional information, please contact: Grandway Group Email: Info@grandway.com Tel: +1 626-357-1200

Commercial real estate investment activity remained robust heading into 2022. Total U.S. commercial real estate investment volume in Q1 2022 was $150 billion, a strong 45% increase from the same period in 2021. The volume in Q1 2022 was quite significantly lower than the $296 billion in Q4 2021, but one must note that Q4 was an all-time historically high volume created by pent-up demand as well as an anticipation of interest rate hikes. Multifamily continued to lead the sectors in investment volume with $57 billion transacted in Q1, up 42% from the same quarter last year. Industrial properties and office were the next two largest sectors with $42 billion in volume in the quarter. Although only at $17 billion transacted in the quarter, the retail section showed strong signs of recovery, showing a strong 87.3% growth compared to the same quarter last year.

When we rank the cities by investment volume in the past 12 months, the top 10 cities are dominated by very large and mature markets led by New York, Los Angeles, and Dallas. Our Fund currently has assets in some of the larger markets as well, including Dallas (3rd at $49bn), Atlanta (5th at $39bn), and Chicago (10th at $25bn). However, what is particularly noteworthy is the next 10 on the list, most of which are markets that this Fund watches very closely and invests quite heavily in, including: Austin (14th at $18bn), Orlando (16th at $14bn), Charlotte (17th at $13bn), Raleigh/Durham (19th at $13bn), Tampa (20th at $12bn). We believe these secondary markets offer more attractive risk and return profiles than the larger and more mature markets. Multifamily and industrial assets are still seeing the most investment for good reason; however, retail investment activity has increased as retail sales continues to recover as U.S. economy opens up.

Persistent inflation has not dampened real estate activity thus far, but the rest of 2022 could prove challenging if current economic concerns persist or worsen. Inflation generally boosts real estate prices in the short term as wages and rents increase, while the counterbalance of higher maintenance and repair costs is slightly muted in comparison. However, prolonged inflation tends to stunt economic growth, so the longevity of inflation is a factor we are observing very closely.

As far as interest rates go, rising rates in the short term can cause dramatic discounts to real estate prices. When the Federal Reserve raises its target rate, that in turn causes market participants to immediately demand a higher % rate of return. This means for the same asset producing the same amount of rent, if the rate of return demanded is higher, the asset’s market price is then discounted as a result. At the same time, the current rate hike is coupled with inflation, which leads to increases in wages and rents, which will likely offset some of the adverse impacts of rate hikes.

U.S. Commercial Real Estate Investment Volume by Quarter

U.S. Commercial Real Estate Investment Volume by Sector

U.S. Commercial Real Estate Investment Volume by Market (Last 4 Quarters)

U.S. Real Estate – Multifamily Market

The multifamily market enjoyed the strongest Q1 absorption in more than two decades, leasing up 96,500 units during the quarter. Typically, the first quarter is seasonally a slow quarter, however, strong pent-up demand in the sector overcame that trend. The continued robust demand for multifamily housing was fueled by a number of factors, including: increased household formations coming out of COVID, job and wage growth due to economic strength and inflation, as well as ever-increasing home prices which drives residents into rental apartments.

The overall multifamily vacancy rate in the U.S. fell to a record-low of 2.3%. This is a compression of 0.2% quarter-over-quarter from Q4, and 2.5% year-over-year from last year’s Q1. This is going to give our property managers the ability to push rents even more aggressively on renewals and new leases.

During the pandemic, the spread in vacancy rates among Class A, Class B, and Class C properties expanded widely compared to historical ranges. Since Class A properties are largely located within more densely populated city centers, many renters escaped those areas to lower density cities, which tended to be mostly Class B and C properties. Many employers during the past two years also allowed workers to work remotely from these Class B and Class C locations, even while these companies maintained their office in the city centers, further supporting the flight to Class B & C. However, in the second half of 2021 we saw a sharp reversion as more companies brought employees back into the office, and the general pandemic concerns subsided. By Q4 2021 and continuing into Q1 2022, the spread now seems to be more “normal” given historical trends, with Class A vacancy rate being approximately 0.5% higher than Class B, and Class B vacancy rate being approximately 0.5% higher than Class C. That said, all three classes of multifamily individually continued to break new lows each quarter.

As a result of historically low vacancy and high inflation rates, average rents increased by 2% quarterover-quarter and 15.5% year-over-year. While this is the trend observed across the country, we operate each of the properties in the portfolio based on its own unique aspects including its location, tenant base, size of units, amenities, etc. At each property, the Fund generally instructs our property managers to prioritize rent growth, both for the purpose of increase rental income as well as potential sale price at exit. However increasing rents too aggressively above what the market can bear, can cause vacancy to rise at the property, which creates a loss of income and negatively impacts future sale price. Therefore, it is a delicate balance we maintain by constantly monitoring rents and vacancy, as well as each individual property’s competition in its submarket.

U.S. Multifamily Vacancy Rate and YoY % Change

U.S. Multifamily Vacancy Rate by Class

U.S. Multifamily Monthly Rent and YoY % Change

U.S. Real Estate – Commercial Retail Market

In the first quarter of 2022, commercial retail market continued to recover. Not surprisingly, in-store sales saw higher increase than online sales as consumer behavior somewhat shifts spending back to physical retail stores. The fear of inflation and potential recession curbed consumer confidence, but nonetheless, strong wage growth and inflation drove overall retail sales up. Not surprisingly, sales of gasoline spiked due to heightened demand and the conflict in Ukraine. Restaurants and bars also saw large increases along with other in-store retailers.

Another point worth noting, is that during the past 2 years, there was minimal new construction of retail properties across the country. This kept the total supply of available retail units, which helps to maintain retail property rent levels.

While the retail sector is not the most critical focus of the Fund, it is important to maintain some diversification. Therefore, retail exposure is kept fairly low in our portfolio, and limited to only certain specific markets.

U.S. Consumer Retail Sales Growth and YoY% Change

U.S. Retail Sales by Category

U.S. Retail Vacancy Rate by Property Type

U.S. Retail Average Asking Rent

Data Sources: CBRE Research, CBRE Econometric Advisors, CoStar Realty Information Inc., Bloomberg, Zillow Group, Redfin

For additional information, please contact: Grandway Group Email: Info@grandway.com Tel: +1 626-357-1200

Heading into 2022, we were cautiously optimistic about the economy and the markets in general. With the health impacts of the pandemic trailing off in the U.S. as a result of high vaccination rates and relatively milder symptoms in the currently dominant strains, the country’s economy had mostly reopened. As the economy reopened, growth was expected to be well above pre-pandemic levels. The switch from a stay-at-home economy to a more normal one was expected to alleviate inflation as the year progressed due to a few reasons. Firstly, the move back to a more normal economy would cause demand for goods to become less concentrated, thereby alleviating pricing pressure on essential goods. In other words, as the economy returns to normal, demand would be spread across more different types of goods, rather than just a few goods that were essential during the pandemic. Secondly, the return to pre-pandemic economy would help to restore the distorted supply chain. Furthermore, the outlook for corporate earnings growth remained robust in Q1. That said, however, there are some concerning factors that we will continuously monitor, including inflation, interest rates, and international factors.

In late February, Russia began its invasion of Ukraine. The invasion has caused a partial damper on this rosy economic view. Many believe there are various motivations behind the invasion, including to restore Russia’s once expansive dominance in Eastern Europe, as well as access to the Black Sea. However, none could reasonably dispute that control of the natural gas in the Donbas region of Ukraine was one of the most significant factors that prompted the invasion. Donbas contains one of Europe’s largest natural gas reserves, and still remains largely untapped due to the high cost of extraction. However, Russia, who is the dominant player in European natural resources, would have no problem extracting those resources and adding them to its assets. Regardless of how the war may end, the invasion will no doubt create turmoil in Europe for years to come. NATO already has and will likely continue to implement sanctions against Russia, but it is unlike NATO will enter the conflict directly as long as the battles are contained outside of NATO countries. The sanctions by NATO and other partners will likely disrupt Russia’s oil exports and drive up fuel costs, as well as disrupt the European economy as a whole.

Inflation in the U.S. seems to be more persistent than President Biden’s administration had anticipated and has by now become the spotlight economic concern. There are no signs of inflation easing in the short term. The U.S. federal reserve, looking to combat the persistent inflation, has begun aggressively raising the federal funds target rate at a faster pace, and to a higher level than previously forecasted. While rates were reduced to near zero during the pandemic, many analysts believe the target rate would be raised to a range of 2-3% during 2022.

The federal reserve is seeking to maintain a good balance between rate hikes, inflation, and economic growth. The agency must increase interest rates sufficiently to combat inflation and the overheating economy, but if this were done too quickly, it may halt economic advances and drive the country into a recession. Or worse, if the rate hikes cool the economy substantially, but do not have enough of an impact on lowering inflation, then the country may fall into a stagflation (a period of economic stagnation coupled with high inflation) similar to the 1970’s, which is far worse than the current environment of high inflation coupled with economic growth.

Despite the concerning factors, the revised outlook by most analysts as of the end of Q1 2022 is not all bad. The U.S. economy is expected to grow robustly as are corporate earnings.

Data Sources: CBRE Research, CBRE Econometric Advisors, CoStar Realty Information Inc., Bloomberg, Zillow Group, Redfin

For additional information, please contact: Grandway Group Email: Info@grandway.com Tel: +1 626-357-1200

Total U.S. commercial real estate investment volume was $296 billion in Q4 2021, bringing the entire year to $746 billion, both of which are record levels. Multifamily led all sectors in investment volume with $136 billion in Q4 and $315 billion for the year. Although Los Angeles. and New York had the highest levels of investment in 2021, Sun Belt markets had the strongest year-over-year growth rates, including Las Vegas, Houston, and South Florida.

Market conditions in commercial real estate improved across the board in the fourth quarter due to various reasons. Solid demand from tenants drove continuous decline in vacancy rates across most property types as well as rent growth. Among all major asset types, office and retail, the two asset types that declined the most as a result of the pandemic, both showed signs of stabilization and continuing rebound. At the same time, industrial and multifamily, two asset types that have experienced soaring demand during the pandemic, have experienced record rent growth with very low vacancy. Demand for industrial properties has been on the rise due to an increase in online shopping and e-commerce as a result of the pandemic, which lead to stronger demand for industrial properties related to production, transportation, distribution, and logistics. This increase in demand for industrial properties outweighed the contraction in the demand for retail sector.

U.S. Real Estate – Multifamily Market

Multifamily demand eased slightly in the fourth quarter of 2021, to 71,600 units, from 185,300 in the prior quarter. Some of this slowdown is a result of seasonal patterns, as the fourth quarter typically is the slowest period each year for apartment leasing. Furthermore, apartment vacancies are low and units are generally hard to find, therefore, rising rents are starting to result in affordability challenges for some households. Net absorption over the past four quarters, which averages out these seasonal differences, came down slightly from the prior quarter but continued to exceed new supply by a ratio of nearly 2:1. Annual net absorption for 2021 was up 238% compared to 2020 absorption and up 97% compared to 2019 absorption.

The rise in multifamily demand during year 2021 was driven by a number of tailwinds. Firstly, household formation as result of pent-up demand was released from COVID lockdowns. Secondly, job and wage growth due to strong economic recovery and continued growth had a positive impact. Furthermore, home prices rose sharply nationwide, causing affordability issues for border-line buyers and driving them towards renting. New York City led all major metros in absorption, emerging out of its overwhelming COVID impact and strict lockdown restrictions. The supply of new unit is also constrained by supply chain issues and a tight labor market as construction costs skyrocketed, so major markets have not been adding supply quickly enough to meet the persistent demand. Overall U.S. vacancy rate for multifamily fell even further by 40 bps from Q3 to a record low of 2.5% in Q4. Noticeably, Class A multifamily experienced the largest decline in vacancy rate to 3.1% by the end of the year, largely due to residents who had previously moved outside of urban centers and are finally moving back. However, Class B and Class C vacancy rates also fell to 2.5% and 2.1%, respectively. Average rent across the nation rose by 2.5% over last quarter to a record $1,950 per month.

U.S. Multifamily Vacancy Rate and YoY % Change

U.S. Multifamily Vacancy Rate by Class

U.S. Multifamily Monthly Rent and YoY % Change

U.S. Multifamily Completion vs. Absorption

U.S. Real Estate – Commercial Retail Market

In Q4, commercial retail properties saw the second consecutive quarter of robust demand, with net absorption of 28 million square feet. In the second half of 2021, commercial retail sector experienced the highest six-month growth in demand since 2016. There has been very minimal new construction of retail properties, keeping supply low. Consumer sentiment continued to fall in Q4 amidst rising inflation and uncertainty about lingering pandemic effects. On the other hand, wage growth remained high as job openings continued to outpace job seekers. The 2021 holiday shopping season turned out strong, with total retail sales increasing by 16.9% over the prior year’s holiday season. Retailers that experienced the largest growth in sales included clothing stores (48% increase largely due to employees starting to return to the stores and increased social gatherings), restaurants (36% increase largely due to higher vaccinations and loosened dine-in restrictions), and gas stations (37% increase largely due to inflation but also a result of more work commute and vacations). Vacancy rate for commercial retail properties fell in Q4 to 5.6%, down 1% from the previous year, partly due to retailers and restaurants finally re-opening after two years of inactivity and partly due to the lack of new supply being built. Rents continued to climb mainly due to a lack of new supply, however, given the backdrop of high inflation, the rent increase seemed fairly minimal.

U.S. Consumer Retail Sales Growth and YoY% Change

U.S. Retail Vacancy Rate by Property Type

U.S. Retail Average Asking Rent

Data Sources: CBRE Research, CBRE Econometric Advisors, CoStar Realty Information Inc., Bloomberg, Zillow Group, Redfin

For additional information, please contact: Grandway Group Email: Info@grandway.com Tel: +1 626-357-1200

The new Omicron variant has spread across the country at an even higher pace than the Delta variant this same time last year. The back-to-back holidays of Thanksgiving, Christmas, and New Year’s, combined with the heightened transmissibility of the Omicron variant, have resulted in a contraction rate of close to 120,000 cases per day at its peak across the country. There also seems to be a large number of break-through cases, especially among those that have been vaccinated twice or fewer. Nonetheless, however contagious the Omicron variant seems to be, the rate of hospitalization and serious symptoms seem to be much lower. Many medical experts believe that this will quickly become the predominant strain in the U.S. Many companies have once again temporarily closed their offices or sent employees home to work remotely.

Despite the presence of Omicron, the U.S. economy grew at an astounding 6.9% annualized rate in Q4, compared to the 2.3% rate in Q3. The economy expanded 5.7% for the year 2021, recording its strongest annual growth since 1984. Unemployment rate fell to 3.9% in December, the lowest level since February 2020, when unemployment rate was 3.5% immediately before the impact of the pandemic began.

The U.S. stock markets rose in Q4, with solid gains across the board, despite a weaker November which was impacted by fears over rising cases of the Omicron variant and the speed of the Federal Reserve’s pullback on federal stimulus. By year-end, these worries had largely subsided, and prevailing data continued to suggest that the economy was stable and corporate earnings were robust. The technology sector, one of the strongest drivers of U.S. economic growth, was one of the best-performing sectors during Q4, as many employees in technology companies were already working remotely even prior to the pandemic and were generally less impacted by the virus. Especially noteworthy were the U.S. semiconductor manufacturers, which posted record profits amidst the global chip shortage. The real estate market as a whole also performed well in Q4, as housing shortage fueled tremendous growth for the residential and multifamily sectors. Commercial real estate, particularly industrials, has experienced excessive demand due to the increase in online shopping and e-commerce, which demand outweighed the contraction in the demand for retail sector.

Data Sources: CBRE Research, CBRE Econometric Advisors, CoStar Realty Information Inc., Bloomberg, Zillow Group, Redfin

For additional information, please contact: Grandway Group Email: Info@grandway.com Tel: +1 626-357-1200

Grandway Residential and Brasada Estates are proud to announce the Welcome Center is officially open! Be amongst the first to experience this private gated community through innovative interactive tools that bring this special community of 65 luxury residences to life

COVID forced multiple 24 Hour Fitness locations into an Chapter 11 reorganization and while other locations closed, Grandway led the prized Texas SuperSport location into a restructure of their lease.